Table of Contents

Introduction

Managing personal finances is crucial for achieving financial stability and reaching long-term goals. Whether you’re saving for a house, planning for retirement, or simply trying to keep your budget in check, effective finance management can make all the difference. In this post, we’ll explore key concepts, strategies, tools, and tips to help you take control of your financial future.

Basic Concepts of Financial Management We Use:

- Budgeting: This involves creating a plan for your income, expenses, and savings.

- Why It Matters: A budget helps you understand where your money goes. It ensures you’re living within your means and planning for the future.

- Savings: Setting aside money for future needs.

- Why It Matters: Investments, emergency funds, vacations, and major purchases all require savings. It provides a safety net for unexpected expenses and future necessities.

- Debt Management: This is about having strategies to handle and pay off debt effectively.

- Why It Matters: Managing debt wisely helps maintain your creditworthiness and reduces financial stress.

Creating Your Personal Finance Strategy

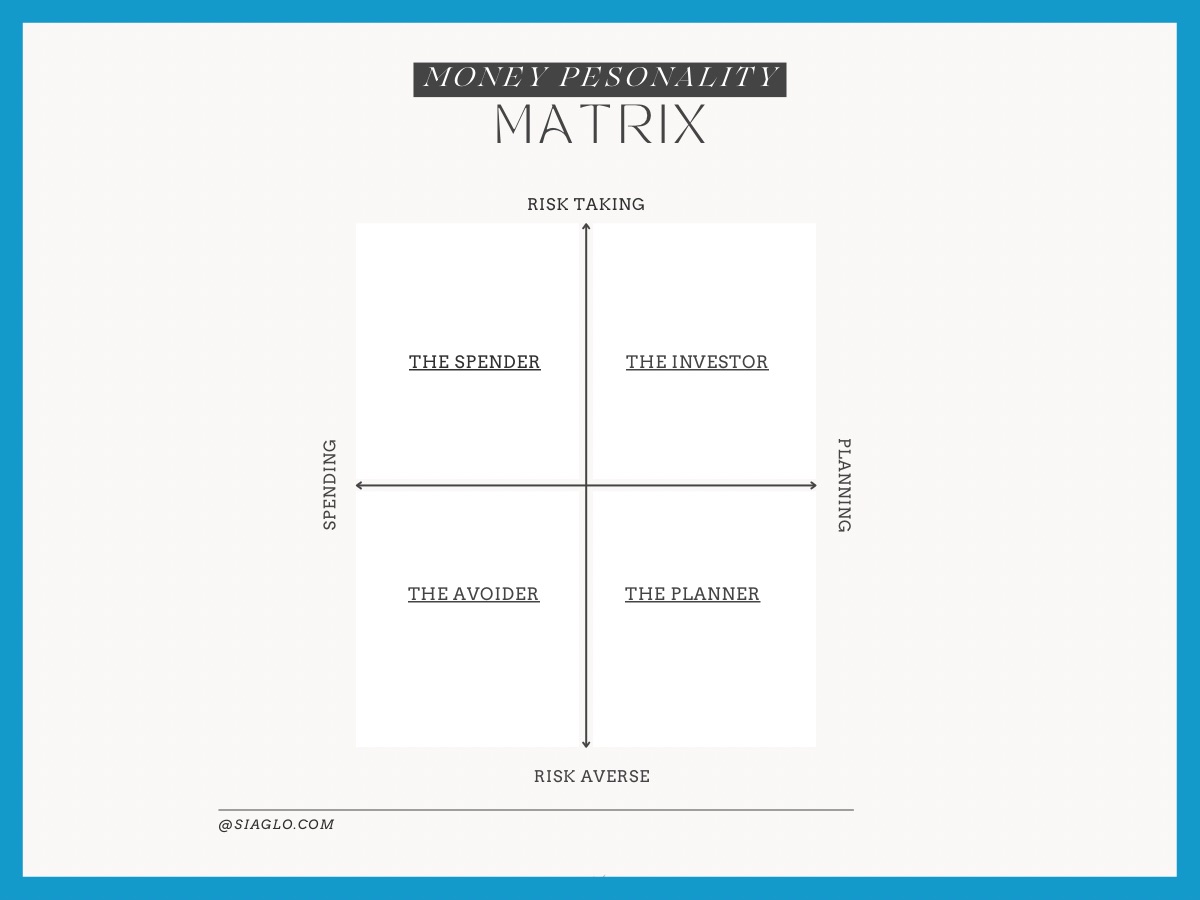

- Understand Your Money Personality

Each personality has strengths and weaknesses and understanding your inherent type helps with why and how money management decisions are made. Recognize your tendency for Risk Aversion vs. Risk Taking and Planning vs. Spending and determine which personality suits you better. Continue to hone in on the strengths and grow yourself in areas of improvement for that personality.

I used the categories below to determine my type. In some situations, you may have to combine more than one personality type to manage. For example, I have to be a planner and investor to manage my long-term savings.

The Planner

- Characteristics: Organized, goal-oriented, detail-focused.

- Strengths: Excellent at creating and sticking to budgets.

- Strategies: Consider taking comfortable risks and ensure long-term goal growth happens.

The Investor

- Characteristics: Knowledgeable, strategic, good at market analysis.

- Strengths: Comfortable with risks and complexities of investments.

- Strategies: Diversified investing, continuous learning and avoiding unnecessary risks.

The Avoider

- Characteristics: Overwhelmed by finances, tends to procrastinate finance management.

- Strengths: Intuitive but disengaged from active financial management.

- Strategies: Simplification, automation, seeking advice.

The Spender

- Characteristics: Impulsive, prioritizes immediate gratification.

- Strengths: Enjoys experiences, good at identifying opportunities.

- Strategies: Setting a discretionary spending budget, using a “fun fund”.

- Assess Your Financial Situation

Start by listing your income, expenses, debts, and savings. This will provide a clear picture of your current financial health.

- Set SMART Goals (Specific, Measurable, Achievable, Relevant, Time-bound).

- Define short-term (saving for a vacation), medium-term (buying a car), and long-term (retirement) goals.

- Ensure there is prioritization within your goals if there are limited funds available (wants vs. needs).

- Choose a Budgeting Method:

Below are some methods. Determine your specific budgeting approach that works for you and use it.

- Zero-Based Budgeting: Allocate every dollar of your income to specific expenses and savings, debt repayment ensuring your budget balances to zero.

- Percent Rule: Allocate x% of your income to needs, wants, savings, charity, and debt repayment. For example, there are budgeting methods such as the 50/30/20 rule. 50% of income for needs, 30% for wants, and 20% for savings. Make sure that you are saving at least 20% of your income. Follow the method you are comfortable with and stick to it.

- Envelope System: Use cash for different categories by placing money in labeled envelopes. Once an envelope is empty, you can’t spend in that category until the next month. I know of a person who uses different bank accounts and credit cards for different types and sticks to the specified amount per month. Use either a digital or physical envelope that works best for your situation.

- Track Your Progress

- Regularly review your budget and goals. Adjust as needed to stay on track, celebrate milestones, and learn from any setbacks.

Tips Based On Our Personal Experiences

- Educate Yourself About Personal Finance

- The more you know, the better decisions you can make regarding your finances. I read somewhere that it takes a minimum of 3 years to learn about stock investments properly. It certainly took me a long time to learn and strategize investments and to avoid some pitfalls. It is still a continuous journey for me.

- Understand stages of wealth to consider your planning.

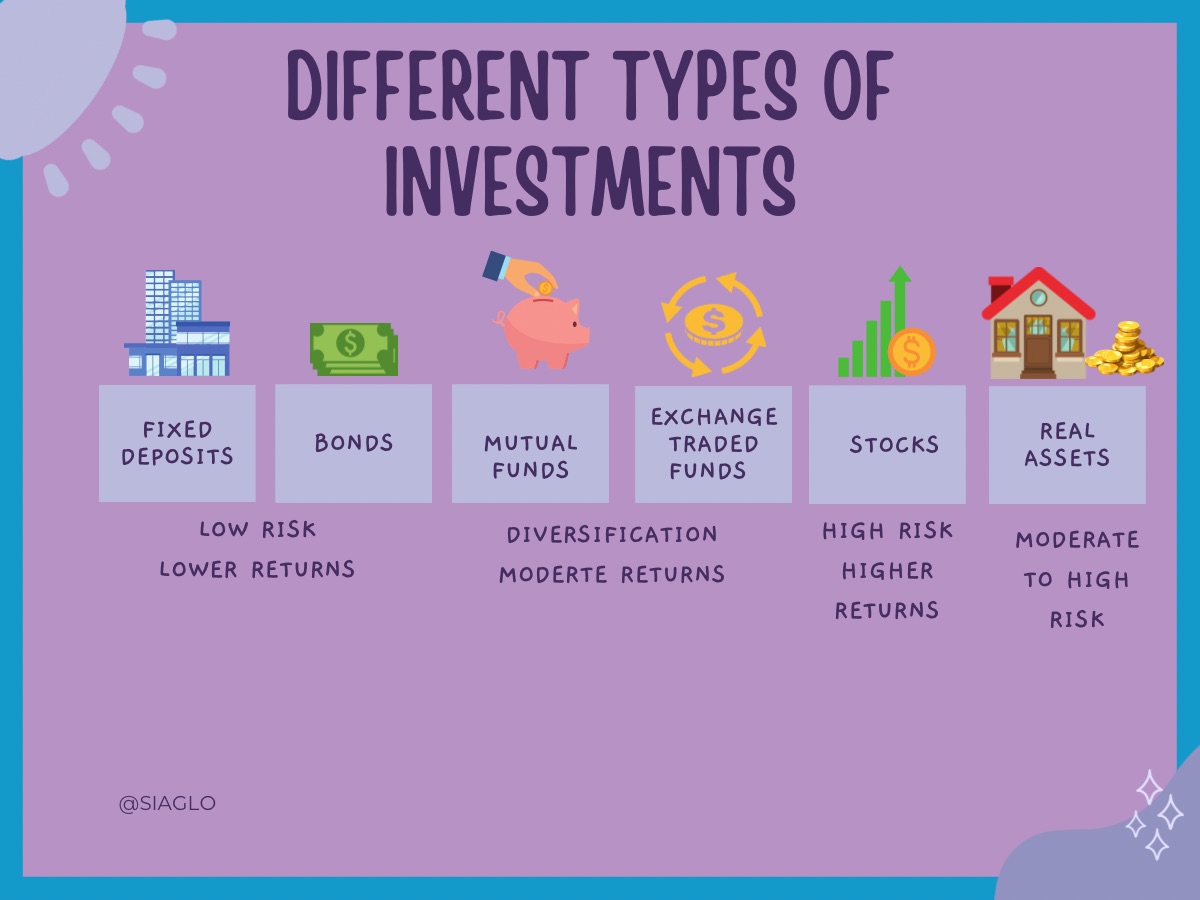

- Understand the Different Types of Investments.

- Start Investing Early to Take Advantage of Compound Interest

- The earlier you start investing, the more time your money has to grow. I can vouch for this method based on my 401K growth. I also invested a very small amount in a mutual fund early in my career. Over the time, the money grew significantly due to reinvestment of gains.

- Save even if it is a small amount but do not procrastinate. Over time, small contributions will add up and benefit from compound growth. When I started my career, I invested $100 per paycheck as that was what I could afford to kickstart my savings and eventually increased the percent contributions as I became more financially stable.

- Pay Yourself First

- Treat savings as a non-negotiable expense. Set aside a portion of your income for savings before paying bills or spending on discretionary items. I invest in a 401K, HSA, and IRA automatically out of paycheck and then take home the remaining amount.

- Arrange for a portion of your paycheck to be automatically deposited into your savings or investment account. This “pay yourself first” approach makes saving effortless. This method works for long-term goals like buying a house, retirement, etc.

- Stay Disciplined and Patient and Practice Consistency

- Financial growth takes time. Stick to your budget, savings plan, and investment strategy, even when it feels challenging. For example, when markets were not doing well, I considered stopping investing. I received advice to take advantage of lower prices and buy more which would be more beneficial in the long run.

- Diversify Your Investments to Spread Risk

I diversified my portfolio not only based on investment types but also based on purpose.

- Use different instruments.

- Investing in a Health Savings Account (HSA) if your plan allows it.

- Start an educational savings account from early childhood for kids.

- Invest across different asset classes (stocks, bonds, real estate, etc.).

- Utilize retirement avenues like 401(k) plans, IRAs, or Roth IRA.

- Invest in Tax-Deferred or Tax-Free Accounts

- Maximize your investment returns by using tax-advantaged accounts like a 401(k), IRA, or Roth IRA. These accounts allow your investments to grow tax-free or tax-deferred, which can significantly boost your wealth over time.

- If your employer offers a 401(k) match, contribute at least enough to take full advantage of that match—it’s essentially free money.

- Invest in a Flexible Spending account to take advantage of tax-free provisions for healthcare. For child care, I used a Dependent Care account and saved a substantial amount in taxes.

- Consider Debt as a Disease

- Either prevent it or pay it off as soon as possible if incurred. Never ever go into debt for “wants”. Always live below your means and understand that “wants” will give you temporary gratification but debt will haunt you for a long time.

- Take Advantage of Employer Provided Benefits

- Make use of voluntary benefits such as pet care insurance, long-term medical care insurance, auto insurance, etc. as you would get group rates and save money.

- I strongly recommend taking advantage of additional life insurance if your employer offers it. Since employers typically provide group rates, the premiums are very affordable, but the coverage can offer significant financial support to your family in case anything happens to you.

- Track Your Finances

- I believe that a person should manage and track their finances no matter how small they are. If this habit is not there, a person can earn millions but they are always financially poor and stressed out. I heard about some sports people or lottery winners going broke due to poor financial management. Start this tracking habit as soon as you start earning. We work hard to make money, we must always put in effort to manage it that includes tracking also.

- Seek Professional Guidance

- If you’re feeling overwhelmed or unsure or have time constraints, consider financial advisor services. When my kids were young and I was juggling professional and home life, I didn’t have time to focus on finance management for long-term goals. At that time, a financial advisor was a better choice instead of letting goals slide.

- List a Beneficiary for Every Account You Own

- Some accounts such as 401 K provide mandatory provisions for beneficiary nominations. Bank accounts and a few others, you need to ensure that the beneficiary is set up because they are optional.

- Assign a Power of Attorney to manage your finances when you are not able to handle them due to physical or mental impairments.

- Create a Finance Binder and Keep it Safe

- Document all your investments, brokerage accounts, bank accounts, retirement accounts, your assets, the last seven years of taxes, and any legal documents. This helps you manage your finance documents easily.

- Evaluate Purchases

- Implement the 24-hour rule: wait a day before buying non essential items to determine if you really need them.

- Before making a purchase, ask yourself if it aligns with your goals and values. Will it bring you joy or serve a purpose?

- Allocate Fun Money

- Set aside a small portion of your budget for guilt-free spending. This allows you to enjoy life while still saving.

Tools for Effective Personal Finance Management

Use your tool of choice. I use Excel to plan and track my budget, investments, and savings. Continuously learn about finances through blogs, podcasts, books, online courses, etc. Don’t procrastinate or avoid documenting your finances. In order to be successful, monitoring and tracking are the key aspects.

Books We Recommend

- The 9 Steps to Financial Freedom by Suzy Orman

- I read this book in my early 30s. Due to this book, I planned my financial well-being which included not only savings but also other important financial aspects such as wills etc. to better prepare for the future. Educate yourself on all aspects of financial management that extend beyond retirement savings and investments.

- Rich Dad, Poor Dad by Robert T. Kiyosaki

- This book taught me about being in a ‘rat race’ if you were to listen to Poor Dad. While parenting my kids, I used to think about this book and ask myself ‘am I teaching like a poor dad or a rich dad?”.

- I will teach you to be Rich by Ramit Sethi

- One word that caught my attention–“No guilt’. This book gave pointers on being smart while enjoying life. It doesn’t talk about cutting small expenses such as coffee to be rich. It advises to be smart by managing the big picture instead of micromanaging day-to-day finances.

- Know Yourself, Know Your Money by Rachel Cruze

- This book talks about seven money tendencies that influence your decisions about money. It helped me understand how my behaviors, values and culture affect my financial actions.

- Various books about Stock investments, mutual funds, and retirement savings

- I believe that my savings should grow and not sit idle and that’s where I rely on investments. To plan for my financial wealth, I learned about investing, retirement savings, and mutual funds. It takes years to learn, so start as early as possible.

Conclusion

Mastering personal finance management is a journey that requires commitment and ongoing education. By understanding the basics, leveraging tools, and crafting a personalized strategy, you can take control of your financial future. Start today, and take every step toward financial freedom!

We love to hear your story about any other techniques that helped you. As always, we are available via SIAGLO Instagram, X, or email.